For me it’s a way of obtaining a discount with your insurance, however it usually only comes up when people get a spike in their insurance premium. If you get a price hike you look for a discount, and then the insurance company suggest you look at having a Wind mitigation. Once the insurance company has the specific details of your home, you get a more personalized for your home and often the specific details are better than the assumed details previously used by the underwriter.

The report looks specifically at 3 areas

1) The most important is the shape of your roof.

2) The attachment of your roof structure to walls and the roof boarding.

3) Age of the Roof

4) Hurricane protected Windows & Doors.

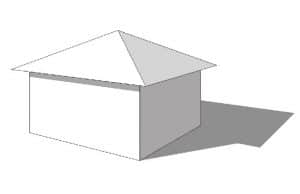

Most people would know if they had a new roof or Hurricane protection. On the contrary the shape and attachment are probably something most people haven’t even though about. Turns out they might benefit you. If you have a roof where the roof slopes down on all sides (rather than having a triangle or gable shape at one or two sides) you are in luck. This would suggest you have a HIP roof and this is an important factor in discounting your roof, but without documenting and informing the insurance company it can’t be taken into account.

HIP Roof and Roof Strap

The report is valid for 5 years, so if you look for the best premium every year this is valid for multiple renewals. In Florida the Hurricane risk is significant, so a significant percentage of the premium is related to Wind related coverage. Consequently, the value of the Wind mitigation is significant.

I can’t speculate on how it would work for individual cases, but I have talked to customers who have had premium spikes. With a positive Wind Mitigation they have managed to get their premium below what they paid prior to price increase. Better to have the money in your pocket than the insurance company’s.